|

|

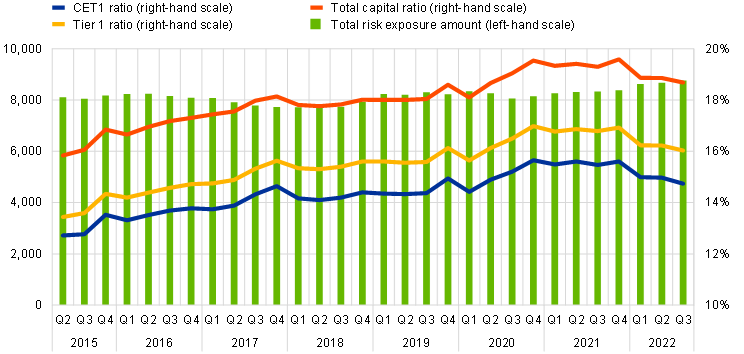

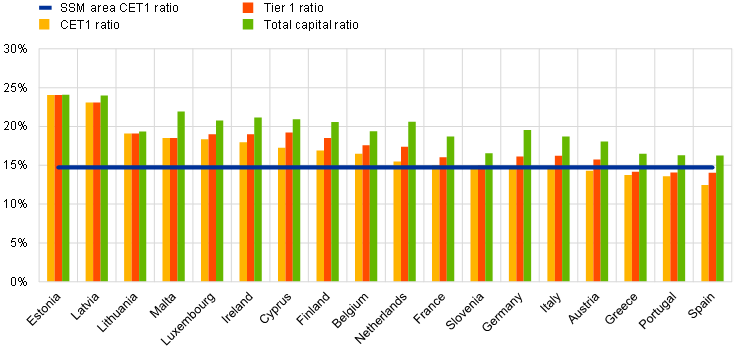

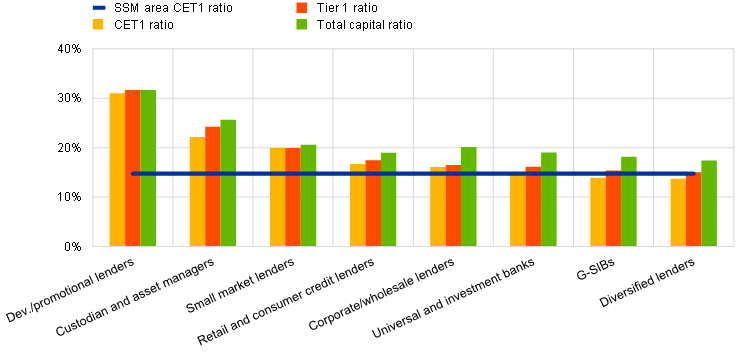

The aggregate capital ratios of significant institutions (i.e. those banks that are supervised directly by the ECB) decreased in the third quarter of 2022. The aggregate Common Equity Tier 1 (CET1) ratio stood at 14.74%, the aggregate Tier 1 ratio stood at 16.03% and the aggregate total capital ratio stood at 18.68%. Aggregate CET1 ratios at country level ranged from 12.48% in Spain to 24.06% in Estonia. Across Single Supervisory Mechanism business model categories, diversified lenders reported the lowest aggregate CET1 ratio (13.74%) and development/promotional lenders reported the highest (31.00%).

Capital ratios and their components by reference period

(EUR billions; percentages)

Source: ECB.

Capital ratios by home country for the third quarter of 2022

(percentages)

Source: ECB.

Note: Some countries participating in European banking supervision are not included in this chart, either for confidentiality reasons or because there are no significant institutions at the highest level of consolidation in that country.

Capital ratios by business model for the third quarter of 2022

(percentages)

Source: ECB.

Notes: “G-SIBs” stands for global systemically important banks. “Dev./promotional lenders” stands for Development/promotional lenders.

The non-performing loans (NPL) ratio excluding cash balances at central banks and other demand deposits decreased to 2.29% in the third quarter of 2022. The decrease was driven by a further reduction in the stock of NPLs to €348 billion (compared with €351 billion in the previous quarter) as well as an increase in total loans and advances (excluding cash balances) to €15,201 billion (compared with €14,962 billion in the previous quarter).

At country level, the average NPL ratio excluding cash balances (green bars on Chart 5) ranged from 0.85% in Estonia to 7.50% in Cyprus. Across business model categories, custodians and asset managers reported the lowest aggregate NPL ratio excluding cash balances (0.62%) and diversified lenders reported the highest (3.40%).

Aggregate stage 2 loans as a share of total loans continued to increase slightly in the third quarter of 2022, reaching 9.79% (up from 9.72% in the previous quarter). The stock of stage 2 loans amounted to €1,434 billion (compared with €1,399 billion in the previous quarter).

Cost of risk stood at an aggregate level of 0.48% in the third quarter of 2022 (down from 0.52% in the previous quarter). Across significant institutions, the interquartile range narrowed further to 0.52 percentage points (down from 0.56 percentage points in the previous quarter).