|

|

Recognising the difficulty in judging the demand for credit in the midst of the COVID-19 crisis, this column focuses on the potential supply of credit and explores the obstacles to ‘usability’ of bank capital. It concludes that the current capital framework falls short: there is not enough ‘usable capital’, and the disincentives to actually draw it down are too strong. Finally, it recommends improvements in current capital framework to overcome these issues.

As COVID-19 spread, policymakers around the world prioritised measures designed to limit the spread of the disease and save lives, but at considerable economic cost. Financial markets have withstood the initial demand for liquidity, but continued credit provision will be crucial as businesses will require funds to tide them through until an economic recovery takes hold. Governments and central banks in many jurisdictions have taken extraordinary steps by guaranteeing emergency loans and easing capital constraints that would otherwise keep banks from lending. But much depends on the actions of banks.

After the reforms that followed the 2008-2009 financial crisis, banks were in much better shape at the start of the COVID-19 pandemic. According to the IMF’s Financial Soundness Indicators, the financial sector’s overall regulatory capital to risk-weighted assets ratio for the US, the UK, France, and Germany were all above 15%, having increased over the previous decade. Regardless, banks were not completely immune to the economic impact of the crisis. Returns were already under pressure pre-COVID-19 (European banks’ returns on assets and equity have fallen over the last decade to below 0.5%), and the current crisis has created new pressures, e.g. use of maintained credit lines by corporate clients has forced banks to acquire more cash (EBA 2020). Against this backdrop, bank managers may reasonably decide to adopt a cautionary stance to protect their balance sheet.

This logic, however understandable, rests on a fallacy of composition. If all banks retrench at once, credit provision would be cut across the board, causing more businesses to fail and amplifying the downturn. Such procyclicality has motivated a set of reforms which included the creation of capital ‘buffers’ on top of capital ‘requirements’ (BCBS 2010). Whereas ‘requirements’ have to be met on an ongoing basis, ‘buffers’ can, at least in principle, be drawn down by banks when needed. But often there is a formal cost to their use: the more banks dig into their buffer the tighter the restrictions they face on paying dividends and bonuses or making share repurchases. The idea is that such constraints force banks to increasingly retain their earnings, keeping these earning available to bolster their capital position (Beck et al. 2020).

The buffer that is explicitly designed to support lending during a downturn is the Basel III countercyclical capital buffer (CCyB) of 0-2.5% of risk-weighted assets. In theory, the buffer is activated during good times (up to 2.5%), nudging banks to accumulate capital that they can draw down in bad times when the buffer is released (down to 0%, or ‘deactivated’). Another buffer, the capital conservation buffer (CCoB) of 2.5% of risk-weighted assets, is also intended to be available for draw down in bad times, but the buffer level is normally maintained and is not designed to vary through time. Together, the CCyB and CCoB should have provided major banks with up to 5% of risk-weighted assets to draw down when the Great Lockdown hit, enabling them to support the economy.

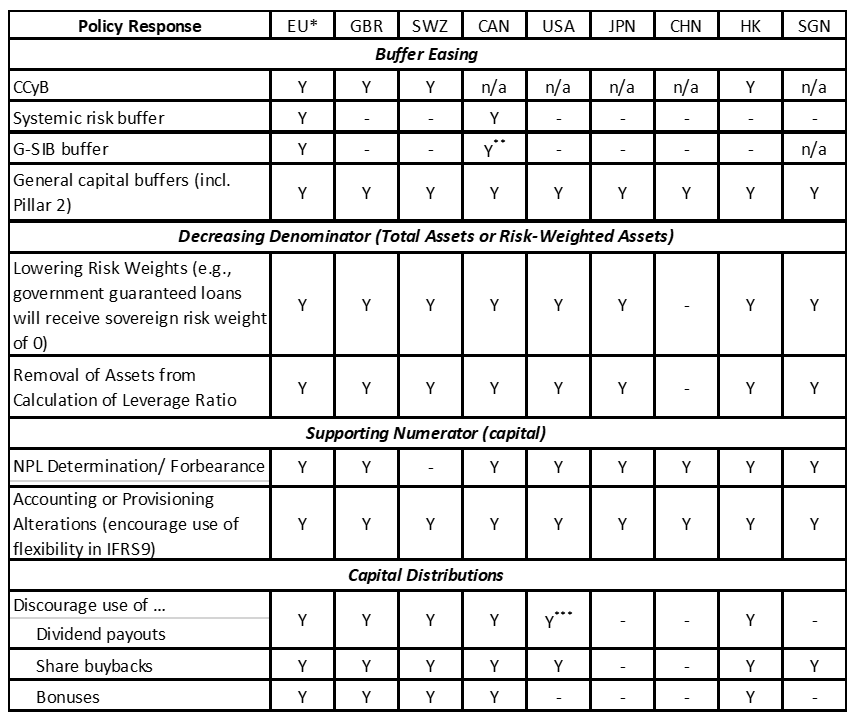

Since the start of the Great Lockdown, regulators and supervisors have taken three types of actions to enable banks to draw down their buffers (Table 1).

1. ‘Deactivated’ (in whole or in part) the CCyB: This was the first-best solution, but the problem was that, despite strong economic conditions, the CCyB had not been raised significantly above 0% in many jurisdictions prior to the Great Lockdown (BIS 2020). In the US, Japan, and Singapore for example, the CCyB stood at 0%, while it stood at only 0.25% in Germany and France. In countries where the CCyB had been raised, such as the UK and Hong Kong, it has duly been released.

2. Expanded the buffer capacity available for banks to draw down through unforeseen discretionary supervisory changes: This included ‘deactivating’ various buffers that were not expressly designed to be releasable in a downturn (BCBS 2010, Drehman et al. 2020). Supervisors and regulators have loosened bank-specific capital add-ons like Pillar 2 requirements and deactivated surcharges such as the G-SIB buffer and the systemic risk buffer.

3. Encouraged banks to make use of the regulatory and supervisory discretion provided and actually draw down their buffers: An important example is the de-coupling of constraints on dividend payments from the use of the buffer, which has taken place in the U S where a hands-off approach (barring undercapitalization results of the upcoming stress tests) is evident.

Table 1 Bank capital-based responses to COVID-19 in selected jurisdictions

Sources: International Monetary Fund, Financial Stability Board, Basel Committee, and websites of jurisdictions’ supervisors and central banks. Information may not be complete.

Notes: CCyB = countercyclical capital buffer; G-SIB = globally systemically important bank; NPL = non-performing loan; IFRS = International Financial Reporting Standards. “n/a” = not applicable, not implemented. “Y” = Yes, affirmatively altered relative to previous supervisory guidance.“-“ = unclear or silent on specific alteration, no obvious official statement found. “*”= EU provides guidance to member states who are expected to implement it. Jurisdictions in the EU often implement the guidance non-uniformly.“**” = Canada has two G-SIBs, which are also Domestically-Systemically Important Banks, where the capital requirements exceeded the minimums so release of D-SIB buffer is sufficient. “***” = If a U.S. bank uses the exclusion of Treasuries and deposits at the Federal Reserve Board from the leverage ratio it needs to request approval for capital distributions. Additionally, the Fed has restricted share buybacks and most dividend distributions during Q3 2020 for large banks following the release on June 25 of the DFAST 2020 (stress test).

These actions have been complemented by guidance that, instead of letting the capital ratio fall directly, is aimed at artificially preserving banks’ capital ratios. Examples include: allowing for a more ‘relaxed’ approach in the computation of risk weights, asset exclusions from the denominator of the capital and/or leverage ratio (by removing government securities and central bank reserves),1 and a more relaxed application of loan loss provisioning (e.g. IFRS-9) that lengthens the timeframe for non-performing loans to be booked.2 The fact that regulators and supervisors have resorted to such backdoor approaches could indicate that they believe that draw-downs using the designated buffers would, on their own, be insufficient or that an obvious fall in capital ratios may endanger a bank’s ability to obtain equity or funding.

We believe both concerns are at play and hence, we see two types of risk. First, the buffer capacity that is available for banks to draw down may be insufficient. This is, for now, hard to empirically evaluate – but there are reasons for concern. Recent research published as a Bank of England working paper suggests that traditional microprudential stress tests would underestimate the buffer levels that are needed. Moreover, the length and depth of the recession given its tie to the literal health of the populace rather than a normal business cycle, make previous estimates of capital adequacy highly uncertain.

The second risk is that, even if buffer capacity were sufficient, banks may not have appropriate incentives to draw them down. Restrictions on dividends and bonuses when buffers are drawn create a disincentive to their use. Blanket dividend restrictions may help to keep money inside the bank and deployable as loans, but banks may instead decide to keep the cash for later payment of dividends and bonuses. In addition, bank management may be concerned that drawing down their buffer will signal to markets that they are in trouble, which (combined with the prospect of limited or non-existent dividends) may hamper their ability to raise equity capital or keep their funding sources (Cziraki et al. 2016). Especially in stressed markets, it is hard to determine ex ante the marked-based threshold of the capital ratio that would retain access to funding, so management may rationally decide not to play it close. Finally, drawing down the buffers to provide credit in a crisis may simply be deemed too risky for the bank, particularly when some central banks are paying interest on the risk-free reserves held with them. Some governments have issued partial or full guarantees for certain COVID-related loans, but even when such full guarantees are in place banks may hesitate to lend due to operational and reputations risks when more businesses fail than normal.

In sum, two design flaws limit the usability of bank capital: maximal buffer capacity is insufficient, and the buffer capacity that exists is not truly usable (or likely to be used). This puts regulators and supervisors in a bind. Either they operate within the existing capital framework, risking a procyclical reduction in credit provision during the Great Lockdown and a deepening of the crisis, or they allow discretionary adjustments and forbearance that could weaken the resilience of the banking system.

Currently, regulators and supervisors in most jurisdictions have chosen the second approach. The risks are clear. First, forbearance makes balance sheets even more opaque, so that it becomes more difficult for investors and counterparties to back out a capital ratio and decide whether a bank is healthy or not. Second, whenever forbearance ends, the solvency issues for banks will be accentuated, perhaps in ways not easily differentiable across banks, which could lead to a systemic funding liquidity crisis. Third, the credit crunch is simply delayed rather than obviated by the inability to take the hits to capital now and recover quickly.

These risks point towards a need to revamp the bank capital regulation framework in order to ensure that there is sufficient usable capital. Although such proposals are a work in progress, we propose three guiding principles:

1. Non-optional build-up of sufficient, usable capital in non-crisis times. As conceptually elegant as the CCyB might be, it did not do its job and should be replaced. Too many jurisdictions opted not to build up buffers despite (relatively) strong economic performance, leaving banks vulnerable at the start of the Great Lockdown. Instead of the CCyB, the CCoB3 – which is fully built-up by default – should be higher and partially releasable immediately in a crisis, with the level calibrated not only to microprudential but also to macroprudential risks (Farmer et al. 2020).

2. Give regulatory discretion to release buffers during a downturn, while providing stronger incentives to actually use usable buffers. To some extent, this will remain a case of pushing a rope (Choi et al. 2019), but more can be done. During a systemic crisis, supervisors and regulators should have the discretion to partially release the CCoB buffer – which is currently not the case4 – without banks facing any payout restrictions, allowing them to discern how to use their buffers most effectively.5 It is notable that US banks have voluntarily cancelled share repurchases and raised loan loss provisions. The part that is not released remains subject to graduated restrictions on discretionary payments, ensuring that beyond a certain point capital is conserved when buffers are being further drawn down.

3. Set clear expectations about the pathway banks should follow to rebuild their buffers. Such expectations should be guided not by the passing of time but by changing (in this case, medical) conditions and be gradual enough that set-backs are unlikely.