CEPR: The market view: What the prices on credit default swaps imply about macroprudential bank buffers in Europe

19 June 2023

This column quantifies systemic risk using data on credit default swaps for European banks. It finds a cluster of large banks with low capital buffers relative to their contribution to systemic risk.

Historically, capital buffers have been recognised as one of the key tools to curb systemic risk and the spillover of shocks from the financial system to the real economy (Sibert 2010, Tente and Düllmann 2013, Altunbas et al. 2017, Mendicino et al. 2021). There is, however, a large disconnect between the academic and regulatory approaches used to evaluate systemic risk. The academic approaches favour the use of market data and asset pricing methods (Huang et al. 2012, Brownlees and Engle 2017, Adrian and Brunnermeier 2016, Acharya et al. 2017). Regulators, on the other hand, rely on balance sheet and regulatory data to generate a score of systemic importance (EBA 2020).

In two recent papers, we address this gap. In the process, we bring to light the risk management role of policymakers. Using bank distress dependencies implied from the credit default swap (CDS) markets, we quantify systemic risk and attribute it to a universe of key individual banks in Europe. This allows us to evaluate the size of the socially optimal macroprudential buffers that banks need to hold. Since capital buffers are one of the main policy instruments for managing banks’ potential contributions to systemic distress, our findings have substantial implications for managing systemic risk in the European Economic Area (EEA).

Risk measurement

First, in Dimitrov and van Wijnbergen (2023a), we develop а framework for measuring systemic risk and attributing it across the universe of European banks based on an approach used in the securitisation industry to model the potential for loss in a portfolio of defaultable loans (Tarashev and Zhu 2006). In that sense, the banking system is modelled as a portfolio of loans and systemic risk measures the potential loss for the sector given that multiple institutions default at the same time.

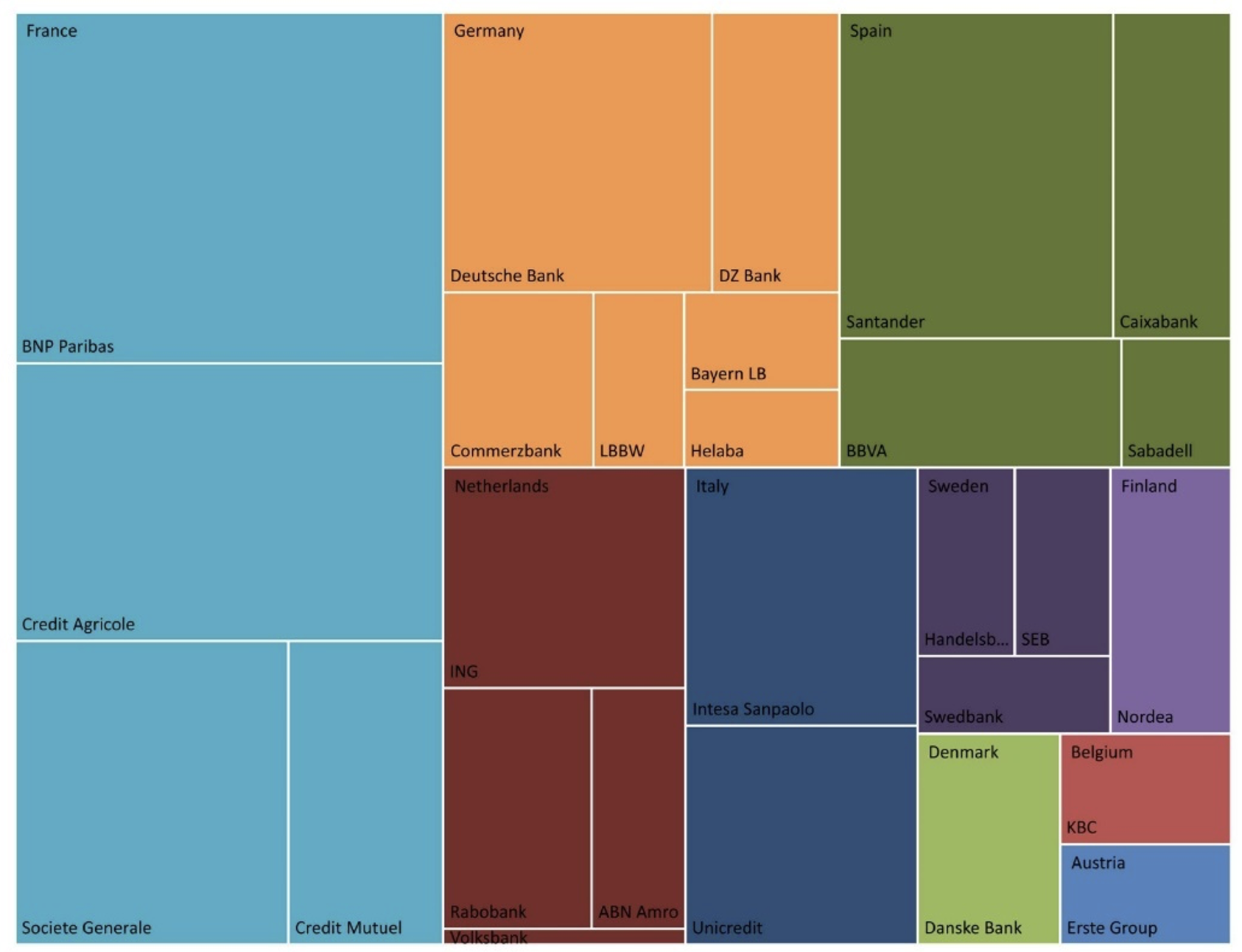

Figure 1 Banks by liability size

In both cases, we use market-driven estimates of systemic relevance. In contrast to the seminal approaches of Adrian-Brunnermeier’s CoVaR (Adrian and Brunnermeier 2016) and Acharya’s marginal expected shortfall (MES) (Acharya et al. 2017) which rely on co-dependencies in the tails of banks’ equity prices, we base our model on a credit risk model calibrated on the prices of single-name credit default swap contracts. This allows us to include in the analysis a number of banks whose equity is not publicly traded, either because they are privately held, cooperatives, or held by the government in some form. Figure 1 shows the full universe that we consider with the area of each rectangle indicating the liability size of each bank in the system.

Credit default swap prices

First, let us discuss what a credit default swap (CDS) contract is. In essence, it is an insurance, which is traded over-the-counter (OTC), and in which the protection buyer agrees to make regular payments – the CDS spread rate over a notional amount – to the protection seller. In return, the protection seller commits to compensate the buyer in case of default of the contractually referenced institution.

There are multiple features of the contract that make it an attractive source of information on the risks which are evolving in the financial sector: the contract directly targets risks of insolvency, it has standardised terms and conditions, better liquidity than corporate debt, a tendency to lead equity markets in price discovery, and prices in government intervention and restructuring of the reference institution. Figure 2 shows the median bank credit default swap spreads per country in our sample and gives us an initial view of the common trends affecting creditworthiness between countries...

more at CEPR

© CEPR - Centre for Economic Policy Research