|

|

This column presents the responses to from three of the Commission’s leading economists.

The European Commission communication for a reform of the EU economic governance framework aims to provide the basis for convergence across Member States on the way forward (European Commission 2022, Buti et al. 2022). It has drawn lots of attention. Most recognise that the Commission has put forward a far-reaching proposal aiming at finding a balance between different views in the complex debate on how the rules should be changed.

In particular, several elements have been considered as important improvements compared to the current rules, most notably (i) taking a medium-term perspective; (ii) increasing the differentiation across Member States based on their debt sustainability; (iii) streamlining the fiscal indicators by focusing on observable net expenditure ceilings; and (iv) integrating better the need for fiscal adjustment with that of supporting investment and reforms (Bordignon 2022, Blanchard et al. 2022).

Certain other features have been met with some criticism. In broad terms, the critical remarks pertain to the institutional aspects, the economic implications and the technical features of the Commission’s approach. Given the attention that stakeholders are paying to the Commission orientations, it appears important to address those misgivings along the three areas just sketched out.

A major criticism that has been emerging concerns the role played by the Commission in the design and assessment of the national fiscal-structural plans (Blanchard et al. 2022, Lorenzoni et al. 2023, Wyplosz 2022), which is considered to lead to a bilateral approach that would undermine transparency and equal treatment. These authors suggest boosting the role of the independent national fiscal councils as a way to ensure national ownership.

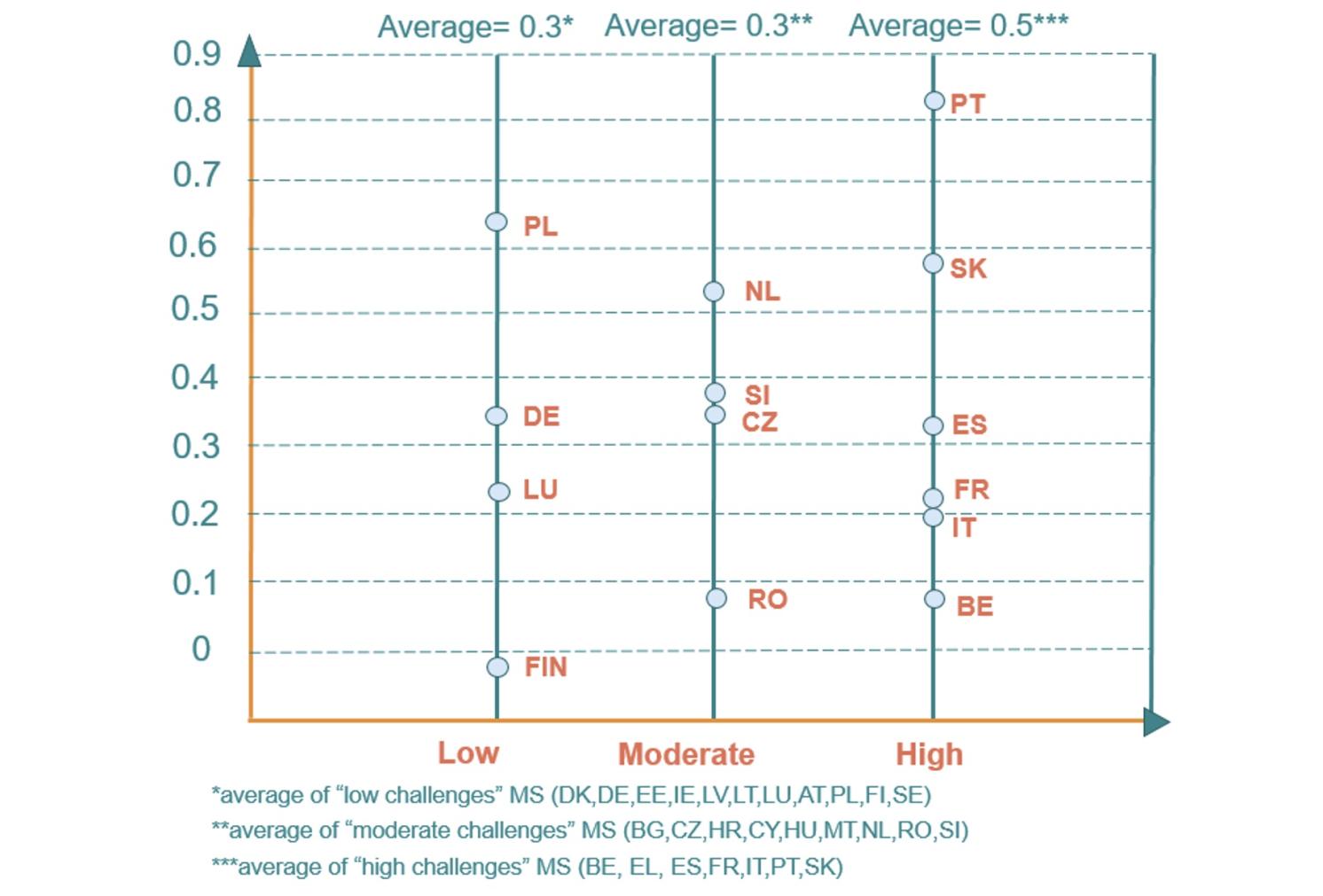

There are two main elements to prevent ‘bilateralism’. First, the Commission will operate within a common EU framework consisting in common requirements that the fiscal adjustment path of a Member State should respect. It is important to stress that, while being common, these requirements would be differentiated on the basis of the Member States’ debt sustainability challenges, which is a major improvement compared to the current system where the requirements and efforts delivered did not sufficiently reflect the actual fiscal consolidation needs. Moreover, there would be common criteria to assess reforms and investment commitments. Second, the role of the Commission ends with its assessment, while the decision on whether to endorse the plans or not lies with the Council, which is a more direct role than the opinion and recommendations by the Council for Stability and Convergence Programmes in the current setting. What the Commission proposes is therefore likely to stimulate the engagement of other Member States and improve the peer review of Member States’ policy plans, including the underlying fiscal and structural policy issues that determine overall public debt sustainability challenges. Gradual and sustained debt reduction is needed, and this will require more fiscal prudence going forward, but as experience shows fiscal consolidation efforts are in themselves not sufficient to ensure a low debt sustainability risk position (see Figure 1).

Figure 1 Debt sustainability challenge and average past fiscal effort (2011-19), selected countries, simple average

Still based on the previous criticism, the Commission could also be perceived as too intrusive when it comes to assessing whether reforms and investment are good enough to justify a more gradual adjustment path. This objection is misplaced because it is up to the Member States to identify a set of reforms and investment that could underpin a more gradual adjustment. In fact, the suggested approach takes inspiration from the existing structural reform and investment clauses, whereby it is for the Member State to commit and provide solid evidence of their beneficial impact, but would make the criteria clearer: the set of reforms and investments should support growth and debt sustainability (in line with the country-specific recommendations as part of the EU Semester); should respond to common EU priorities; and should be sufficiently detailed, frontloaded, time-bound and verifiable.

An objection pertains to the role of the reference paths to be put forward by the Commission at the outset of the process, which could be seen as undermining political ownership by Member States of their fiscal adjustment strategies. The reference paths should not be seen as quantitative minimum requirements computed and imposed by the Commission. Nor they should be seen as providing a maximum fiscal effort. They are, instead, a practical translation of the common requirements that is meant to provide concrete guidance to Member States before they prepare and submit their own plans. To strengthen the common EU framework and the accountability of the Commission when assessing the plans, the methodology for determining these reference paths would be fully transparent and would be made public.

Finally, the Commission intends to strengthen the role of the independent national fiscal councils which were created via a directive on national fiscal frameworks. These institutions will play a greater role in assessing the assumptions underlying the plans, providing an assessment on the adequacy of the plans with respect to the debt sustainability and the country-specific medium-term goals, and monitoring compliance with the plans.