|

|

A big geopolitical strategy gain with a small economic gain

Today, international trade policy is increasingly geopolitically volatile. Within that context, in the Indo-Pacific region, there are three significant plurilateral configurations.[1] One is the CPTPP, which is a Free Trade Agreement (FTA) of like-minded countries promoting an open and rules-based trading system. The Regional Comprehensive Economic Partnership (RCEP)[2] is a more development-friendly and shallower FTA in comparison to the CPTPP which includes China.[3] The Indo-Pacific Economic Forum (IPEF) is not an FTA but a policy forum negotiating trade-related rules.[4] It is led by the US where a strong motivation is the containment of China.

For the UK, the significance of the CPTPP should thus be seen in the context of a wider foreign geopolitical strategy beyond trade. In the UK’s latest Integrated Review 2023,[5] the Government reaffirmed the importance of the ‘Indo-Pacific tilt’, for which the CPTPP provides a core policy framework. The CPTPP could enable the UK to enhance strategic ties with like-minded countries to protect a free and open Indo-Pacific region.

Yet, the economic value for the UK is likely to be small. On the face of it, the CPTPP looks to create new opportunities for the UK given the size of the market (11% of the world’s GDP, US$14.3 trillion; 14% of world exports and imports of goods and services, US$7.5 trillion). However, the predicted long-term economic gains for the UK are but a possible 0.08% increase in GDP.[6] The UK already has bilateral FTAs with nine CPTPP members out of eleven,[7] including ‘comprehensive and deep’ bilateral FTAs with its top four CPTPP trade partners (Japan, Canada, Singapore, Australia)[8].

What price will the UK pay?

While joining the CPTPP may be a geopolitical strategic gain, it is important to be mindful of the economic and social consequences. These will depend on the final agreement. Consider two examples.

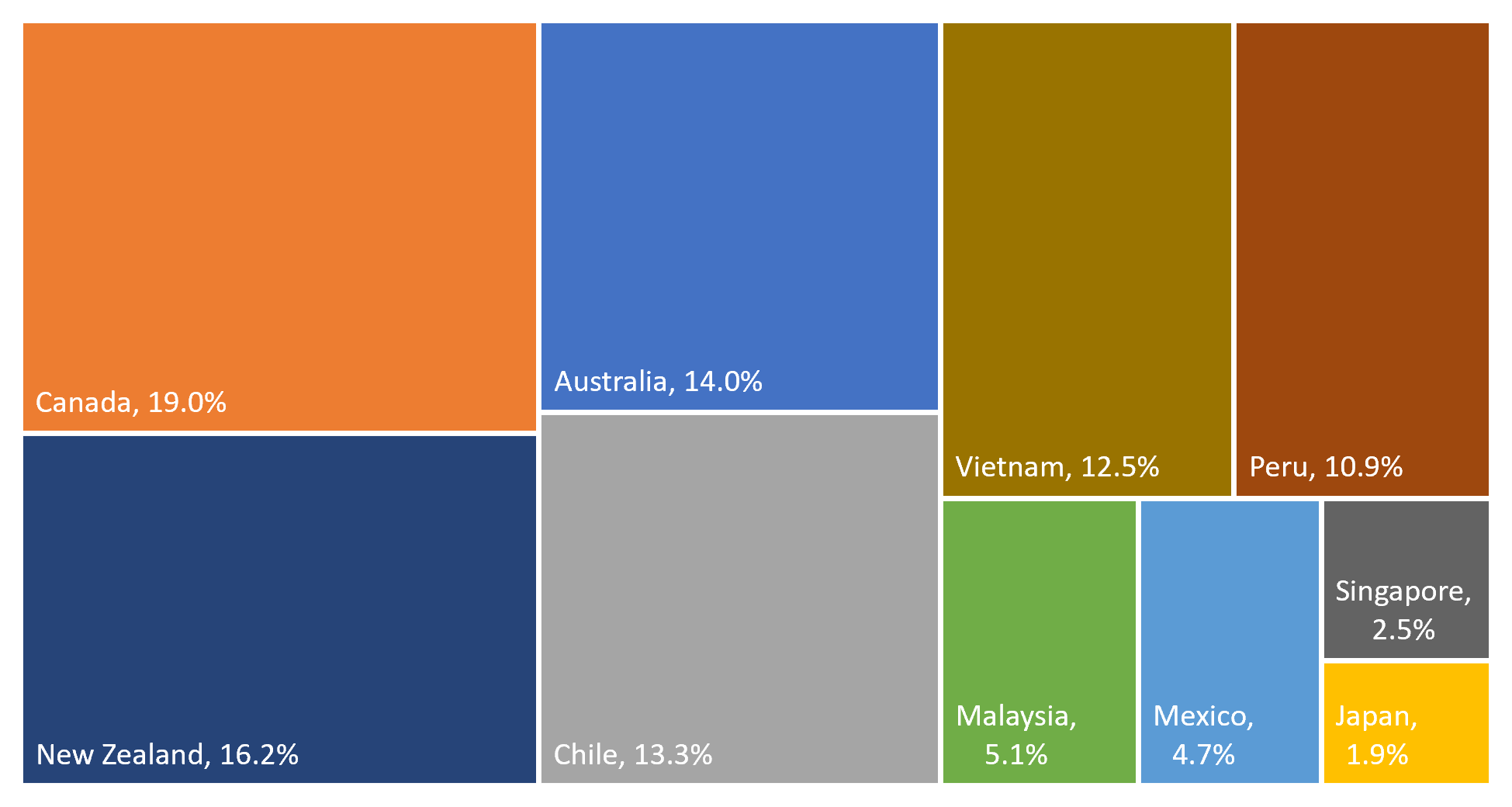

Take first the UK’s agricultural market access concessions. The CPTPP has its own schedules of market access commitments which in principle apply to all members, hence the UK cannot differentiate its commitments by country. Canada is the largest CPTPP agricultural exporter to the UK (Fig.1). A critical issue is whether the UK grants the same levels of market access as it already has for Australia and New Zealand under its bilateral FTAs to all CPTPP members. Depending on the arrangements, an increase in imports of some products (e.g. beef, sheep meat and dairy products) may impact on UK agriculture. [9]

Figure 1: Agriculture & Agri-food exports from the CPTPP members to the UK (£) -2021

Data source: HMRC Overseas Trade Statistics, 2021.

Note: Shares are out of CPTPP total exports of agriculture and agri-food products to the UK. Agriculture and agri-food products are defined as those under HS Chapters 01-24.

Second, consider regulatory policy constraints. The UK has different regulatory regimes and norms in comparison to Indo-Pacific countries, however, accession requires acceptance of existing CPTPP rules. UK stakeholders have expressed concerns that some provisions may create economic, legal, societal and technical problems both at the domestic level and for the UK’s relationship with the EU.[10] Examples include free cross-border data flow (CPTPP Art. 14.18) and its potential impacts on data privacy and the EU’s data adequacy decision;[11] incompatibility between the CPTPP intellectual property provisions (CPTPP Art. 18.83) and the UK’s membership of the European Patent Convention; the UK’s ability to maintain the precautionary principle for agriculture and food standards (CPTPP Art. 7.9 (2))[12] and animal welfare standards; and Investor-State Dispute Settlement (ISDS) mechanisms (CPTPP Chapter 9: Section 9B) and its regulatory chilling effects in the areas of environment, labour and health.[13]...

more at UK TPO