In the face of the COVID-19 crisis, massive purchases of government bonds by the ECB through its Pandemic Emergency Purchase Programme, or PEPP, were crucial for averting a financial crisis. However, as a side effect, the PEPP diminishes even further the supply of euro denominated safe assets available to other central banks.

This creates a conundrum for the ECB. If it continues buying government bonds to support the euro area economy, it limits the availability of assets for use as foreign exchange reserves by central banks still further. Based on Eichengreen and Gros (2020), we propose a way out: the issuance of ECB Certificates of Deposit (ECBCDs).1

Strengthening the international role of the euro

Strengthening the international role of the euro is official policy of EU institutions. According to its 2020 work programme, the European Commission intends to adopt a strategy of “Strengthening Europe’s Economic and Financial Sovereignty”. The ECB has similarly embraced this aim (Panetta 2020).

One measure often used to gauge the international role of the euro is its share in foreign exchange reserves. This share is in the range of 20% to 25%, or about one third of that of the US dollar. It is often argued that the euro’s share is so low because there do not exist enough euro-denominated safe assets (e.g. Valla 2019, Habib et al. 2020). Reserve managers, the argument goes, prefer to invest in low-risk, liquid government bonds. In practice, an AAA/AA rating is needed to qualify for safe asset status. Only four euro area countries have this rating (FR, DE, NL and AT), and their combined marketable debt of €5 trillion is dwarfed by the close to $20 trillion of US Treasury bonds outstanding.

Moreover, until now, there has not existed a significant supply of safe common euro area assets. The fiscal measures adopted by the EU and its member countries hold out promise that this supply might now increase. However, any such tendency is being offset by the ongoing asset purchases of the Eurosystem.

ECB bond buying and the supply of safe euro assets

Between 2014 and 2018, the ECB purchased roughly €2.2 trillion of government bonds under the PSPP. Roughly 60% of this was spent on the bonds of the four countries supplying safe assets. Since these bonds are now held by the Eurosystem and are no longer on the market, this has effectively reduced the scope for international investors to hold euro assets.

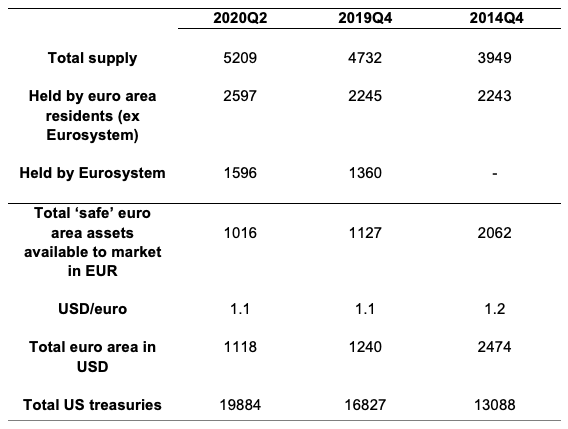

Table 1 shows the impact of the PSPP up to now: a drop in the marketable amount of about €1.4 trillion between 2014 and 2019. (The total includes supranational bonds of €200 billion.)

In addition, European banks are required to hold ‘high-quality liquid assets’ in proportion to their balance sheets, for which public sector bonds are their main source. Hence another significant fraction of euro area public debt securities is absorbed by the banks (about €1.5 trillion by end 2019). Together with other euro area sectors (insurance, etc.) amounts available for international investors, such as reserve managers, were limited to €1.1 trillion at end-2019 (fourth row of Table 1).

The PEPP initiated in March 2020 constitutes an extension of the PSPP. So far this year, the supply of safe government bonds available to global reserve managers has actually declined (from €1.1 to €1.0 trillion) because the Eurosytem and other euro area residents have been buying safe assets more quickly than governments have issued them.

Looking forward, the €1.35 trillion of additional purchases planned by the ECB (equivalent to 12% of euro area GDP) over the next 18 months are larger than the expected deficits of euro area member states over the same period.

The continuing operation of the PEPP will also reduce the supply of common safe assets expected from the Next Generation EU financial package of support to member states. The Eurosystem is likely to purchase as much as half of the (maximum of) €850 billion of common bonds that the EU is planning to issue.2 The additional net supply of euro safe assets may thus increase only by about €425 billion (equivalent to 4% of global reserve holdings).3

Table 1 Stock of debt securities outstanding available for the rest of the world (not held by euro area residents)

Note: As supplier of safe euro assets to the market,

we considered the AAA euro area countries (Germany, France, the

Netherlands, and Austria) and the supranationals. To obtain the amounts

displayed in the table we proceeded on three steps. First, from the

Government Finance Statistics (GFS) we retrieved the total amount of

debt securities outstanding for the suppliers of safe assets considered,

for June 2020, December 2019, and December 2014. Second, from the

Securities Holding Statistics (SHS) we retrieved data on the total

amount of debt securities issued by the governments of the safe assets

suppliers mentioned above and held by euro area residents for 2020Q2,

2019Q4, and 2014Q4. These data series do not include the debt securities

held by the Eurosystem, so we considered the PSPP and the PEPP

breakdown history database, to obtain cumulative data until June 2020

and December 2019 on the securities issued by the safe assets suppliers

under analysis and held by Eurosystem under PSPP. Finally, we subtracted

from the total outstanding amount of debt securities, both the amount

held by the Eurosystem under PSPP and PEPP (if applicable) and the

amount held by euro area residents. The numbers on the first four rows

are expressed in billion EUR, the numbers on the last two rows are in

billion USD.

Source: Own calculations based on ECB

Statistical Data Warehouse (Securities Holding Statistics, PSPP

breakdown history and Government Finance Statistics) and TreasuryDirect.

How to increase safe assets

The ECB (or rather the Eurosystem) finances its bond purchases by issuing bank deposits. These deposits are not tradable outside the banking system (central banks can’t hold them as foreign reserves). Thus, the PEPP reduces the supply of euro safe assets to the market and enlarges bank balance sheets, on both counts making it more difficult for central banks around the world to invest their reserves in euros.

We propose a simple solution to this conundrum: the ECB should make its liabilities tradable. The easiest way would be for the ECB to issue tradable Certificates of Deposit (ECBCDs). ECBCDs would constitute a euro area safe asset par excellence. They would be an attractive way for foreign central banks to hold reserves in euros, provided of course that the certificates in question can be traded globally and are issued in a sufficiently large amount to create a liquid market.

One would not need to invent a new legal basis for this instrument.4 Item 4 of the balance sheet of the Eurosystem is 'debt certificates issued'. The ECB’s own definition for this item is as follows:

“ECB debt certificates’ means a monetary policy instrument used in conducting open market operations, whereby the ECB issues debt certificates which represent a debt obligation of the ECB in relation to the certificate holder”.

ECBCDs would be attractive because they would not be bottled up in the euro area banking system. Normally only banks (officially monetary financial institutions, or MFIs) are entitled to hold accounts with the ECB or the National Central Banks of the Eurosystem. The legal provision governing the assets in these accounts is clear:

“The ECB shall not impose any restrictions on the transferability of ECB debt certificates”.

This implies that there would be no legal obstacle for a foreign central bank to acquire ECBCDs.5

Neither would market size be a problem. At present,6 liabilities to banks are some €3 trillion euro for the Eurosystem as a whole. This suggests that the ECB could easily issue €1 trillion in ECBCDs without having to worry that this amount would have to be reduced in the foreseeable future.

The present legal basis for ECBCDs limits their maturity to 12 months, which might limit their attraction. IMF data show that central banks hold about $1.5 trillion of reserves in the form of deposits, with about two thirds held at other central banks and one third held at commercial banks. ECBCDs should constitute an attractive substitute for deposits held at euro area national central banks (or even deposits at the Bank for International Settlements). This should ensure a small but significant market for short-term ECBCDs.

However, the market for medium maturities is evidently much larger. McCauley (2020) shows that Treasury bills (with a maturity of less than one year) account for only about 1/10th of total Treasury holdings (with bonds constituting the remainder). The Swiss National Bank reports that the average maturity of its fixed-income investments is over four years. All this indicates that it would be important to offer foreign central banks an instrument with a maturity of several years.

One concern with the ECB in issuing longer-dated CDs is that such issuances would make it difficult to reverse the asset purchases or to reduce lending to banks. However, the balance sheet of the Eurosystem is unlikely to shrink even if the current crisis is overcome. The ECB is granting loans of three years to banks under the targeted longer-term refinancing option (TLTRO). There is thus little danger that the amount of ECBCDs outstanding could be larger than lending to banks and the amount of assets held, suggesting that it should be possible to issue three-year ECBCDs.

One objection to this proposal is that issuing these certificates could be seen as draining liquidity from banks, which could be interpreted as a tightening policy. But the counterpart of the issuance of tradable ECBCDs would be lower deposits at the ECB which carry a negative rate and thus diminish bank profits. Although this problem has been partially addressed by the tiering of the deposit rate, it could be reduced further, thus alleviating the tax on bank profits implicit in negative deposit rates and make the monetary stance more effective. One could therefore argue that the issuance of ECBCDs is entirely compatible with the ECB’s primary mandate of maintaining price stability (as well as its subsidiary mandate of supporting the general policy of the EU).

Conclusions

Large-scale bond buying under the PEPP reduces the supply of safe euro assets to the market. This effect could be neutralised, at least in part, were the ECB were to issue its own Certificates of Deposit.

The legal framework for issuing Certificates of Deposit already exists. The ECB could immediately issue between €2 trillion and €3 trillion of ECBCDs, thereby significantly increasing the supply of euro safe assets to the market and helping to internationalise the euro.

Authors’ note: Angela Capolongo is now working at the European Stability Mechanism (ESM). This column was completed before she joined the ESM. The views expressed here are solely those of the authors and are not to be reported as those of the ESM.

References

Eichengreen, B (2011), Exorbitant Privilege: The Rise and Fall of the Dollar and the Future of the International Monetary System, Oxford University Press.

Eichengreen, B and M Flandreau (1996), “Blocs, Zones and Bands: International Monetary History in Light of Recent Theoretical Developments”, Scottish Journal of Economics 43(4): 398-418.

Eichengreen, B (2016), “The future of the international monetary and financial architecture”, Conference proceedings.

Eichengreen, B, A Mehl and L Chitu (2018), How Global Currencies Work, Princeton University Press.

Eichengreen, B (2020), “Dollar Sensationalism”, Project-syndicate.org, 12 August.

Eichengreen, B and D Gros (2020), “Post-COVID-19 Global Currency Order: Risks and Opportunities for the Euro”, Study for the Committee on Economic and Monetary Affairs, Policy Department for Economic, Scientific and Quality of Life Policies, European Parliament, September.

Hardy, D C (2020), “ECB Debt Certificates: the European counterpart to US T-bills”, Department of Economics Discussion Paper No. 193, University of Oxford.

McCauley, R N (2020), Safe Assets and Reserve Management, Chapter 8 in J Bjorheim (ed.), Asset Management at Central Banks and Monetary Authorities, Springer International Publishing.

Panetta, F (2020), “Unleashing the euro’s untapped potential at global level”, Member of the Executive Board of the ECB, Meeting with Members of the European Parliament, 7 July.

Habib, M M, L Stracca and F Venditti (2020), “The Fundamentals of Safe Assets”, ECB Working Paper no.2355, January.

Valla, N (2019), “Safe Assets in a Monetary Union”, Presentation to the CEPR Research and Policy Network on European Economic Architecture, 16 April.

Endnotes

1 Previously, Hardy (2020) also proposed the introduction of the ECB certificates, that could serve as counterpart to the short-term US assets, such as T-bills.

2 The (self-imposed) limit of Eurosystem holdings of national government bonds is one third. For so-called ‘supra-national’ debt it is half. Close to one half of ESM bonds are held by the Eurosystem (though not by the ECB as a legal entity). Supra-national bonds are important for national central banks that could not otherwise buy their share of national debt because they would exceed the one-third limit.

3 Another unknown is the size of bank balance sheets and their demand for sovereign debt. If households continue to accumulate bank deposits but the demand for credit remains weak, banks will have little choice but to accumulate even more government securities (which have a zero risk weight). Over the first six months of 2020, commercial banks increased their holdings of Euro Area government debt securities by more than €300 billion, an amount similar to purchases by the Eurosystem (somewhat more than 400 billion).

4 The legal base for this instrument was created in 2015 and can be found here (2.4.2015 EN Official Journal of the European Union L 91/21 ).

5 Certificates of Deposit are not unusual instruments for a central bank to issue. A case in point is Denmark, where the interest rate on certificates of deposit is the central bank’s main policy instrument. In the Danish case this instrument is very short term: loans to banks and CDs have the same maturity, namely one week (https://www.nationalbanken.dk/en/monetarypolicy/instruments/Pages/Default.aspx). The Swedish national bank also uses certificates of deposit as its main policy instrument.

6 August 2020 (https://www.ecb.europa.eu/press/pr/wfs/2020/html/ecb.fst200804.en.html)