|

|

Western nations have imposed severe sanctions on Russia in response to its invasion of Ukraine. The most immediately disruptive sanctions targeted the Russian financial system, impairing Russia’s ability to trade internationally and freezing around half of its nearly $600 billion foreign reserves.

Critics of these sanctions argue the West is self-sabotaging, for example by reneging on the institutional promise that Western central banks will always honour claims against them and by politicising Western financial systems. They argue Russia, and other countries wanting to insure themselves against Western sanctions, will simply use their own currencies and payment systems, making future sanctions less effective.

On cue, Putin has announced that Europe must now pay for Russian gas with roubles rather than euros. At the same time, Russia is pushing India to start paying for its gas in euros rather than dollars. This illustrates Russia’s dilemma: it cannot escape Western currencies. Western critics of financial sanctions miss a crucial point. To retain their international position, the West’s financial institutions and currencies do not need to be apolitical. They just need to be less politicised than the alternatives.

Russia’s trade depends on Western currencies

Start

with how Western sanctions harm Russia’s trade. US financial sanctions

excluded Russia’s largest bank, Sberbank, and the Russian central bank

from clearing payments in US dollars, and froze the US assets of other

important Russian banks. The US sanctions make it harder – though not necessarily impossible –

for Russia to deal with US dollars. Any cross-border transaction in US

dollars will, at some point, use a US intermediary bank and rely on US

settlement systems, and therefore be susceptible to US sanctions.

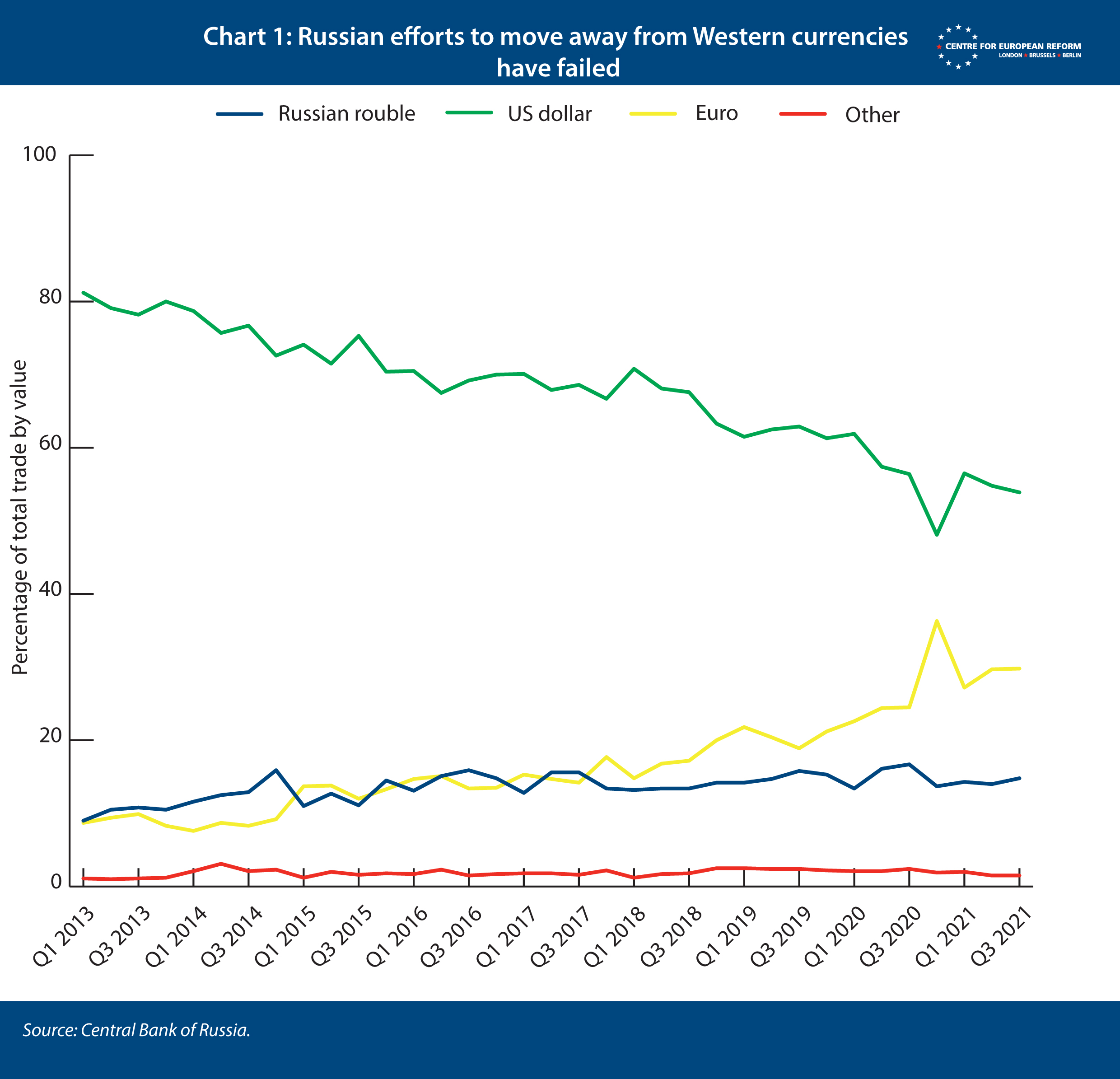

Russia has long been aware of the risks of using US dollars for its trade. It has successfully promoted the rouble’s use in transactions with other members of the Commonwealth of Independent States (CIS) like Belarus. However, Russia has not, until now, insisted on using the rouble for trade outside the CIS. As Chart 1 shows, Russia’s global trade has been invoiced increasingly in euros in recent years instead, leaving the total share of Russia’s trade in Western currencies practically unchanged.

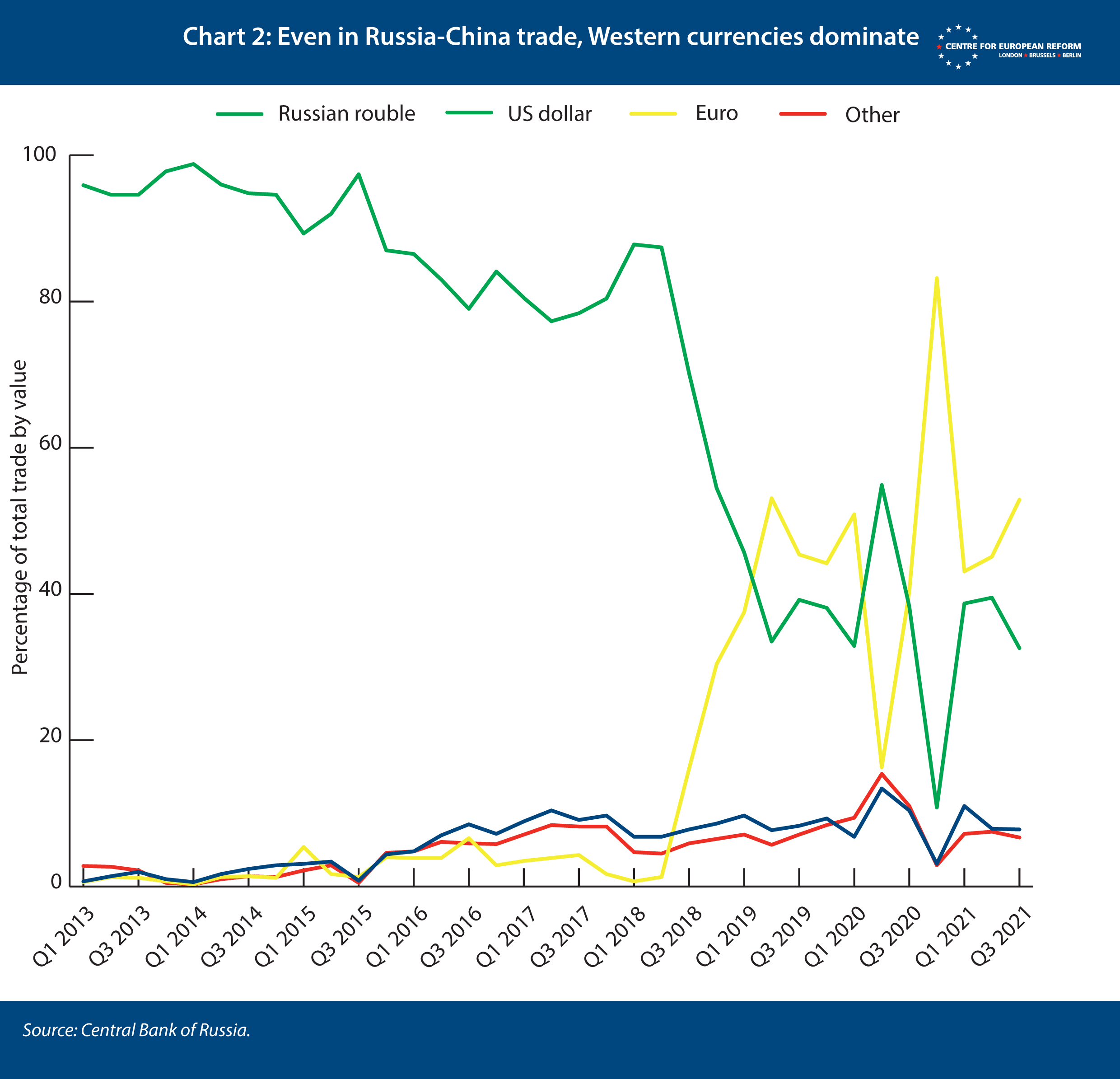

As Chart 2 shows, this trend is true even in Russia’s trade with China – despite China’s own ambitions to increase the international role of the renminbi and a 2019 agreement between Russia and China to settle their bilateral trade in renminbi or roubles.

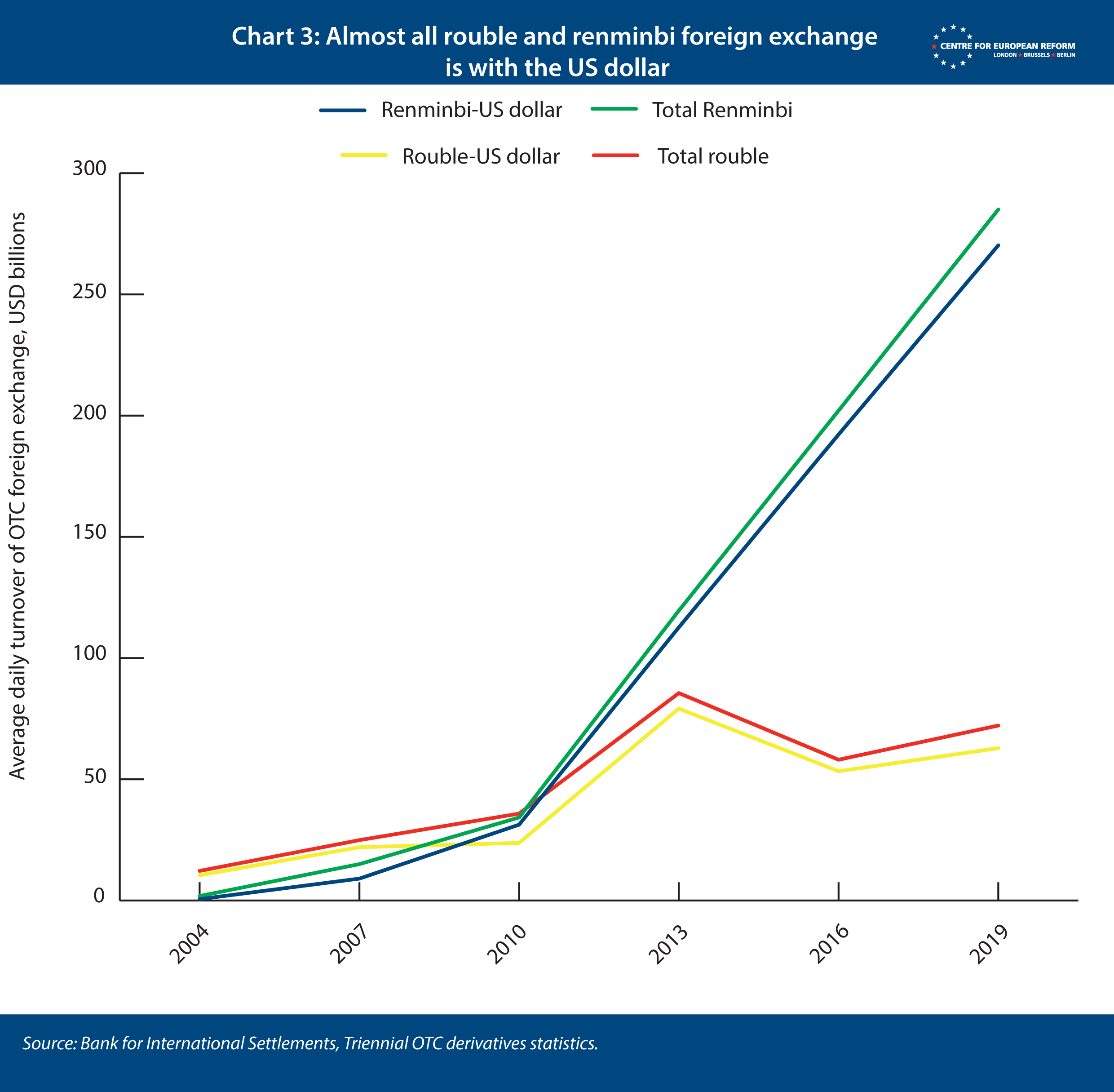

Russia pivoted to euros rather than renminbi or roubles because trading in renminbi or roubles would cost Russia more and reduce its choices. As Chart 3 shows, nearly all currency exchange involving roubles or renminbi are conversions to or from the US dollar. Even euros are much less liquid: 95 per cent of renminbi foreign exchange trades were to or from US dollar, whereas only just over 1 per cent were to or from the euro. Transactions between lesser-used currencies are rare and often performed ‘synthetically’, using the US dollar as an intermediary.

Russia pivoted to euros rather than renminbi or roubles because trading in renminbi or roubles would cost Russia more and reduce its choices.

Tweet thisAs a result of Russia’s sanctions-induced crisis, China has tried to increase rouble–renminbi currency trading. Unlike most Western economies, China normally tightly manages exchange rates with its trade partners. But it has let the rouble plunge in value against the renminbi. This should have facilitated greater exchange volumes (though it will cause hardship for Russians, who will be less able to afford Chinese imports). Despite this, trading between renminbi and roubles is still pricey. The difference between bid and asking prices on rouble-renminbi trades recently widened to 0.0287: more than five times higher than the typical equivalent figures for converting US dollars to euros. This means there are still very few renminbi–rouble trades occurring, compared to dollar–rouble or euro–rouble trades, and the rouble’s real value cannot be easily assessed.

Against this background, Putin’s demand that Europe pay for gas with roubles seems to be grandstanding. European governments have so far refused Putin’s demand to pay for gas with roubles. Even if they agreed, this would only had Putin a symbolic victory. Unless Russia is trying to increase its revenues by using an artificial exchange rate, it would be better off with payments in euros, which it can force exporters to convert to roubles as necessary to maintain the value of the currency. This is why Russia has just asked India to pay for gas not by using roubles, renminbi or rupees – as has been constantly speculated in recent weeks – but in euros.

Russia and China’s alternatives are not credible ...more at CER