|

|

Recent strains at some banks in the United States and Europe are a powerful reminder of pockets of elevated financial vulnerabilities built over years of low rates, compressed volatility, and ample liquidity.

Such risks could intensify in coming months amid the continued tightening of monetary policy globally, making it especially important to understand and safeguard this broad swath of the financial sector that comprises an array of institutions beyond banks. Nonbank financial intermediaries, including pension funds, insurers, and hedge funds, also play a key role in the global financial system by providing financial services and credit and thus supporting economic growth.

The growth of the NBFI sector accelerated after the global financial crisis, accounting now for nearly 50 percent of global financial assets. As such, the smooth functioning of the nonbank sector is vital for financial stability.

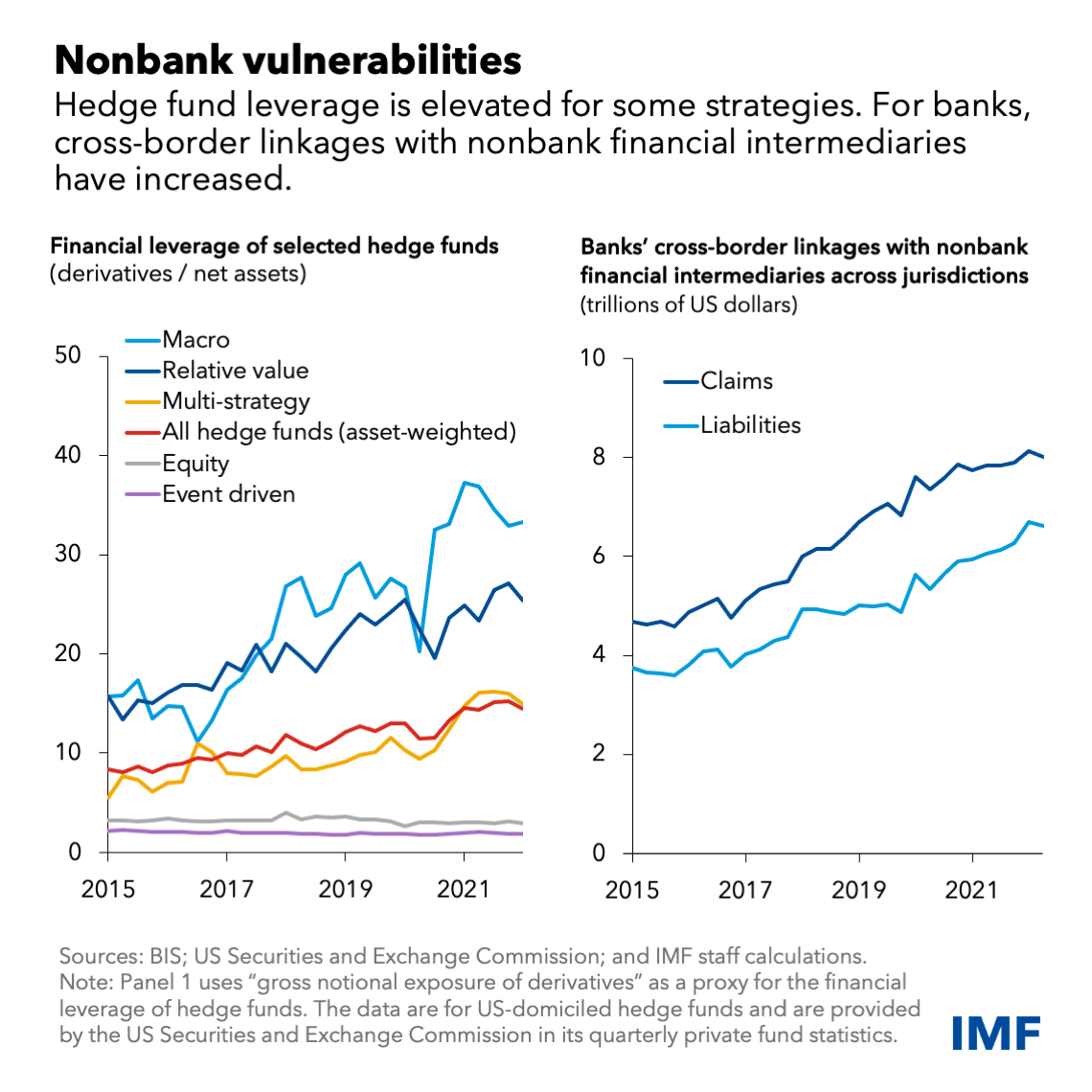

However, NBFI vulnerabilities appear to have increased in the past decade. As we show in an analytical chapter of the latest Global Financial Stability Report, NBFI stress tends to emerge alongside elevated leverage, for example borrowing money to finance their investments or boost returns, or using financial instruments, like derivatives.

Stress is also brought on by liquidity mismatches, where an institution is unable to generate sufficient cash either through liquidation of assets, such as bonds or equities, or use of credit lines to satisfy investor redemption requests.

Finally, high levels of interconnectedness among NBFIs and with traditional banks can also become a crucial amplification channel of financial stress. Last year’s UK pension fund and liability-driven investment strategies episode underscores the perilous interplay of leverage, liquidity risk, and interconnectedness. Concerns about the country’s fiscal outlook led to a sharp rise in UK sovereign bond yields that, in turn, led to large losses in defined-benefit pension fund investments that borrowed against such collateral, causing margin and collateral calls. To meet these calls, pension funds were forced to sell government bonds, pushing their yields even higher.