|

|

When it comes to financial stability, the world is facing a split screen of short-term and medium-term factors. The good news is that near-term financial stability risks remain contained.

Why? Because the likelihood of a soft landing for the global economy has significantly increased. As inflation continues to decline, major central banks have started cutting interest rates. This is boosting already buoyant asset prices and keeping financial market volatility subdued.

At the same time, our latest Global Financial Stability Report calls on policymakers to remain vigilant about the medium-term prospects. We want to highlight two areas of concern.

Concerns Down the Road

For one, accommodative financial conditions have continued to increase vulnerabilities, such as lofty asset valuations around the world, increased government and private-sector debt levels, and more use of leverage by financial institutions, to name a few. All this could amplify future shocks to financial systems. We have seen vulnerabilities mount before, most notably ahead of the 2008 global financial crisis. The build-up is usually gradual, which should give policymakers time to adjust.

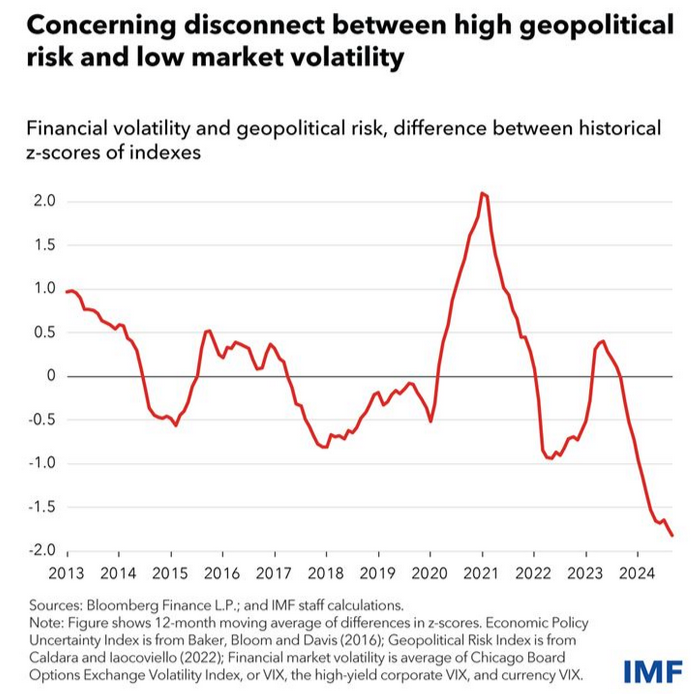

The second area of concern is the disconnect between heightened uncertainty—especially related to increased geopolitical risks—and financial market volatility. A standardized measure of volatility has drifted far below geopolitical risk measures. This indicates that asset prices may not fully reflect the potential impact of wars and trade disputes. Such a disconnect makes shocks more likely, because high geopolitical tension could trigger sudden sell-offs in financial markets and prompt volatility to snap back as it catches up to uncertainty. In that case, some financial institutions may be forced to sell assets or deleverage balance sheets to meet margin calls or satisfy risk limits. While such actions may protect individual institutions, they can actually exacerbate market sell-offs.