|

|

This power of the ECB was conceived in the SSM founding regulation as one of the preconditions for European banking supervision to be credible and impactful. In particular, our sanctioning power is expected to foster a culture of prudential compliance among institutions subject to European regulatory requirements and the ECB’s supervision.

That is why sanctions are part of the ECB supervisory toolkit, together with enforcement measures which, unlike sanctions, can only be used when a breach of prudential requirements is still ongoing. The aim of these tools is threefold.

First, they contribute to effective supervision: direct enforcement powers help the ECB ensure and restore compliance with prudential requirements. This, in turn, creates confidence in the soundness of the banking system and promotes its stability.

Second, they stop banks benefiting from breaching prudential requirements: non-compliance should not provide undue benefits to banks, including competitive advantages.

Third, and very importantly from a prudential forward-looking point of view, the deterrence penalties discourage banks from committing similar breaches in the future, which promotes a compliance culture in the banking system and thus contributes to its stability.

In the European context there are a number of challenges for the implementation of a compliance culture. First, the previous fragmentation of supervisory jurisdictions implied different approaches to compliance. For example, some jurisdictions were more likely to impose sanctions, while others perhaps preferred other types of interventions. Second, the enforcement and sanctioning legal framework can be complex in certain instances, especially in terms of the interplay between European and national laws and powers.

Against this background, this blog post aims to clarify the framework in place for the exercise of the ECB’s enforcement and sanctioning powers in the area of prudential supervision. More specifically, it focuses on the recent publication of the ECB Guide to the method of setting administrative pecuniary penalties.

Let us begin by recalling which prudential requirements are under the supervision of the ECB. We are entrusted with ensuring banks comply with prudential requirements in the areas of own funds, capital requirements, large exposure limits, liquidity, leverage and reporting, and the public disclosure of information on those areas. These requirements are laid down in directly applicable EU law, such as the Capital Requirements Regulation (CRR).

In addition, we are tasked with ensuring that banks comply with prudential requirements in the area of governance, including fit and proper criteria, risk management, internal controls and remuneration policies and practices. These requirements are laid down in national law implementing the Capital Requirements Directive (CRD).

The scope of our enforcement and sanctioning powers in banking supervision is, therefore, limited to breaches identified in the abovementioned areas. In contrast, the supervision and enforcement of the requirements imposed on banks in the areas of consumer protection or anti-money laundering fall exclusively under the remit of the national authorities. The ECB cooperates with those authorities to ensure a high level of consumer protection and to fight against money laundering. In our prudential assessment, we also consider the shortcomings identified in those areas when they reveal failures in banks’ internal control and governance arrangements. However, the ECB has no enforcement or sanctioning power to ensure compliance with consumer protection or anti-money laundering rules.

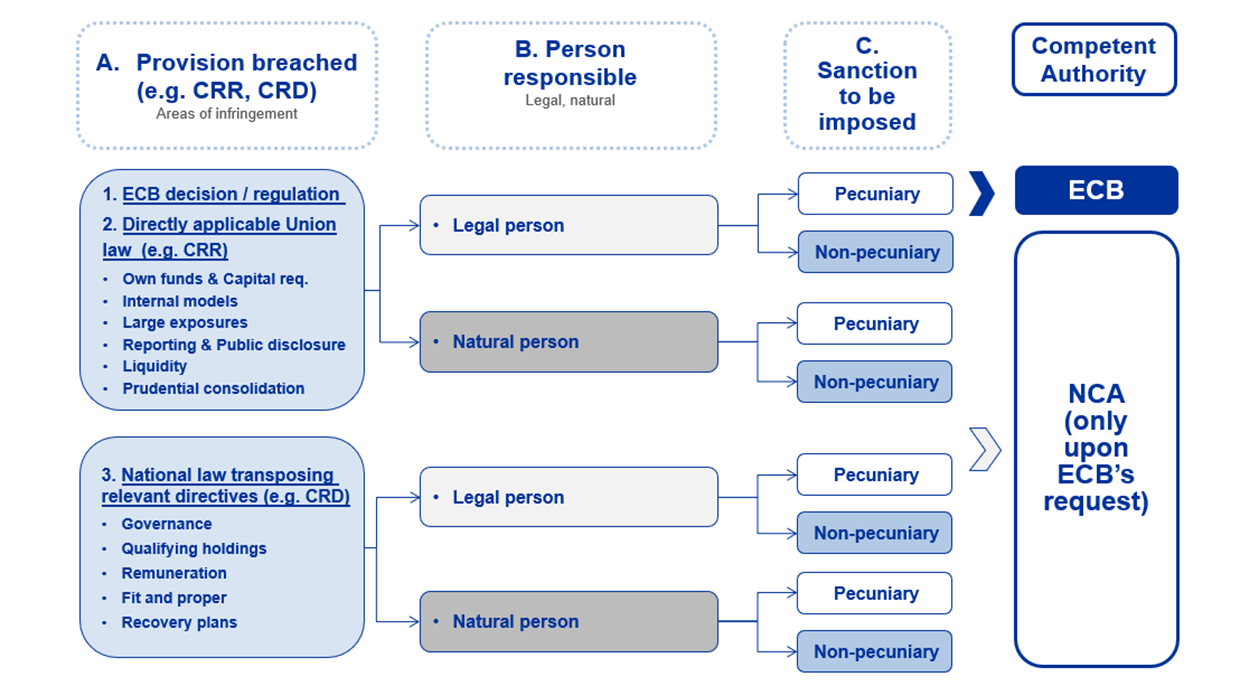

The allocation of sanctioning powers within the framework of the SSM is complex, as it depends on three different elements: (i) the type of provision breached (i.e. directly applicable EU law or national law implementing directives imposing prudential requirements); (ii) the persons responsible for the breach (i.e. legal persons or individuals); and (iii) the type of penalty to be imposed (i.e. pecuniary or non-pecuniary).

The ECB can sanction both significant and less significant institutions in the event of breaches of ECB regulations or decisions. In addition, we can sanction significant institutions for breaches of directly applicable EU banking law (e.g. the CRR).

The direct enforcement and sanctioning powers of the ECB are limited to pecuniary penalties imposed on legal persons. In other words, the ECB cannot directly impose other types of penalties, such as a public warning, on legal persons, nor can it sanction natural persons in any manner.

To ensure the effectiveness of these powers throughout the banking union, the ECB is entitled by law to request that the national competent authorities (NCAs) open proceedings. This may happen in three situations. First, in the case of breaches of national law implementing directives (e.g. the CRD). Second, if the ECB considers that non-pecuniary penalties, as provided for in national laws (i.e. a public warning), should be imposed. Third, if the ECB considers that natural persons should be sanctioned. NCAs remain fully competent to impose sanctions on both significant and less significant institutions in the case of breaches of national law not implementing EU directives or of national law implementing EU directives unrelated to the ECB’s supervisory tasks.

Figure 1

Allocation of sanctioning powers within the SSM: significant institutions

Source: ECB Banking Supervision

As soon as we identify shortcomings in a bank, we may adopt supervisory measures, such as capital add-ons, restriction of business or operations, divestment of activities that pose excessive risks to the bank’s soundness, restriction or prohibition of dividend distribution, ask the bank to reinforce its governance arrangements, etc. These measures focus on preventing breaches and aim to ensure that banks address their weaknesses at an early stage.

While supervisory measures are initiated by Joint Supervisory Teams (JSTs), enforcement and sanctioning measures are handled by the ECB’s Enforcement and Sanctions Division (ESA), which is an independent unit in ECB Banking Supervision. As ESA is not involved in day-to-day supervision, suspected breaches of prudential requirements are normally identified by the JSTs or other relevant business areas responsible for the direct and indirect supervision of banks, who then refer these suspected breaches to ESA for further investigation.

In addition, any European citizen can contribute to the identification of breaches. If you are a bank customer or employee who suspects that your bank has breached EU banking supervision law, you can share your suspicions with us via our whistleblowing platform, which is also operated by ESA. The ECB never reveals the identity of a person who makes a report without first obtaining that person’s explicit consent, unless such disclosure is required by a court order. We are also constantly improving the security of our platform and its technical capacities. For example, we offer European citizens the possibility to report suspected breaches of prudential requirements in several languages, and we continue to expand the number of languages available on the platform.

As soon as a suspected breach is identified and referred to ESA, it conducts all the necessary investigation to clarify the facts and relevant circumstances of the case, including those relating to the impact of the breach and the level of misconduct of the bank. For this purpose, ESA may request documents and explanations. It may also examine books and records, conduct interviews and exercise other investigatory powers if necessary.