ESMA Report Confirms BETTER FINANCE Findings of Investor Detriment through “Fixed Fee Splits” in Securities Lending

10 June 2022

Three years after its first report, BETTER FINANCE expanded on its research into securities lending[2] to once more find that fund managers’ “fee split” arrangements, particularly with in-house agents, vary considerably and may be contrary to ESMA’s Guidelines.

A report published on Tuesday

31 May 2022 by the European Securities and Markets Authority (ESMA),

confirms BETTER FINANCE’s findings that fund managers often don’t seem

to act in the best interest of fund investors when it comes to

securities lending.

Three years after its first report,[1] BETTER FINANCE expanded on its research into securities lending[2] to once more find that fund managers’ “fee split”[3] arrangements, particularly with in-house agents, vary considerably and may be contrary to ESMA’s Guidelines.[4] Such practices could lead to investor detriment and actually constitute a breach of the generally duty of care[5] towards “retail” fund investors.

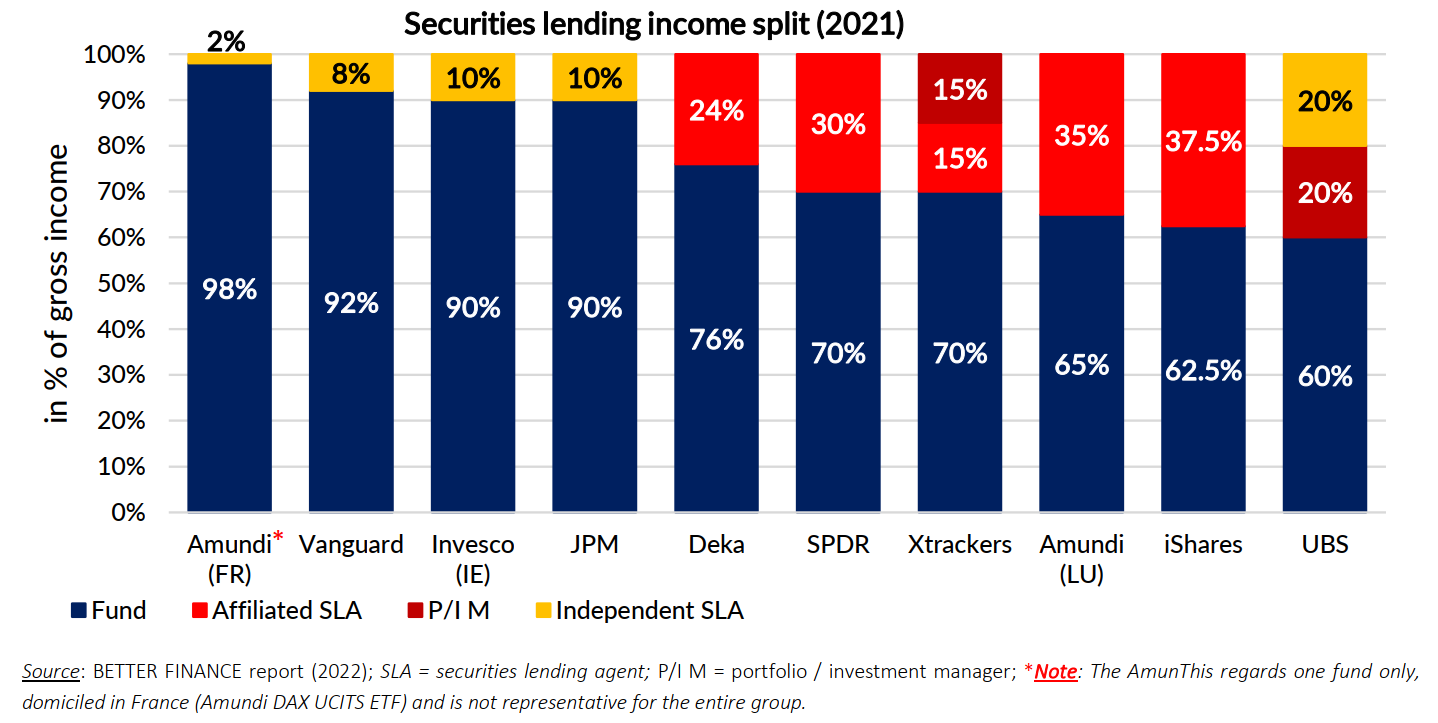

EU “soft”[6] law stipulates that securities lending income, net of direct and indirect operational costs,[7] must be returned to the funds’ beneficial owners.[8] The key provision is that these operational costs cannot include “hidden revenues”,

reason for which BETTER FINANCE questions why some asset managers can

pay as little as 2% of gross income, while others deduct up to 40%.

Read the full press release below.

[2]

The practice of lending a stock, bond or other financial instrument in

exchange for interest, with our focus on EU equity UCITS exchange-traded

funds (ETFs).

[4] European Securities and Markets Authority, Guidelines on ETFs and other UCITS issues (Guidelines for competent authorities and UCITS management companies, 1 August 2014) ESMA/2014/937EN, available at:

[5] According to MiFID [Art. 24(1)], and the UCITS V Directive [Art. 14(1)(a)], fund managers have the obligation to “act fairly, honestly, and professionally in accordance with the best interests of clients”.

[6]

This is because ESMA’s Guidelines and Recommendations are not directly

enforceable and must be transposed into national law by national

competent authorities, or otherwise explain why not (comply or explain principle).

[7] Which cannot include “hidden revenues” for asset managers.

[8] ESMA Guidelines on ETFs and other UCITS issues, para 28.

Better Finance

© Better Finance